The U.S. agricultural sector suffers from abnormally high levels of concentration, giving just a handful of corporations a virtual chokehold over food production and consumption. This has forced hundreds of thousands of independent family farmers off the land and damaged rural economies, public health and our environment. Efforts to restore fairness and competition in agriculture are long overdue and could transform the landscape of our food system for the benefit of all, not just a few.

American Agriculture is Severely Concentrated

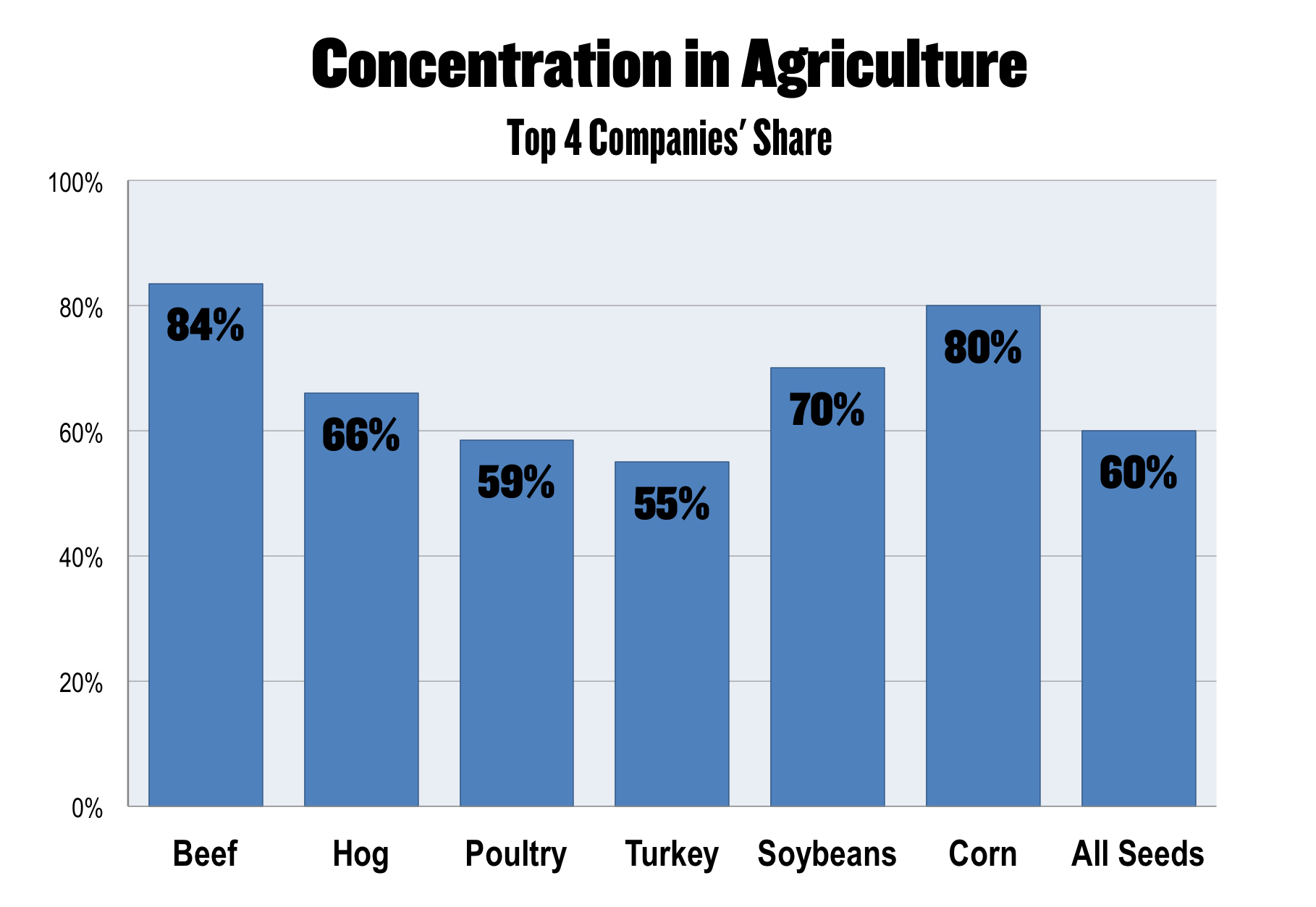

Farmers have never seen as consolidated a market as the one today, both for the inputs they need to keep their farms running and the markets where they sell their goods. Most economists state that if the concentration ratio (CR) for an economic sector – or the market share of the top four firms in an industry – is above 40%, competition is threatened and market abuses are more likely to occur. The higher the number, the bigger the threat. In agriculture, concentration ratios far exceed this level for nearly every commodity.[1]

Unchecked corporate power distorts markets and leaves farmers and ranchers vulnerable to abuse and unfair practices. For consumers, unchecked corporate power means higher prices and less choice. Food costs have risen steadily since the 1980s, while the farmer’s share of the retail food dollar has plummeted by 50%. Because of their market power, corporations can push down the prices paid to farmers without passing on their savings to consumers.

Livestock & Poultry Markets

At the turn of the 20th century, the U.S. passed a series of groundbreaking laws to address monopolies, anticompetitive conditions and abusive practices in the marketplace. These laws – the Sherman Antitrust Act and Clayton Antitrust Act – were written in the time of oil barons and railroad tycoons when it became clear that laissez-faire capitalism was threatening the public good and laws were needed to prevent companies from accumulating and exerting excessive power. While these laws are critical for several economic sectors, they don’t address specific factors in agricultural markets and the dynamics farmers face in the marketplace.

In 1921, the Packers and Stockyards Act (PSA) was created to regulate meatpackers, livestock and poultry dealers, swine contractors and other middlemen in the livestock industry. The PSA addresses industry-wide concentration and anticompetitive practices in the livestock sector, but also contains several provisions that protect individual farmers and ranchers from abuse and unfair practices. Almost every transaction that occurs between farmers and meatpackers is influenced by the PSA, meaning that the vast majority of meat and poultry we consume is touched by this law.

The PSA is meant to level the playing field and reign in the power of corporate meat giants. But, implementation and enforcement of the law has been severely lacking for decades, and more recently, thwarted by the lobbying muscle and deep pockets of corporate meatpackers.

Antitrust Enforcement at the USDA

The USDA’s Grain Inspection, Packers & Stockyards Administration (GIPSA) is charged with enforcing the PSA to foster fair competition in agriculture, protect farmers from deceptive and fraudulent practices, and curb corporate abuse. GIPSA has a checkered history of regulatory inaction, but this turned around during the Obama Administration.

The 2008 Farm Bill authorized new authority for GIPSA to issue stronger protections for farmers and ranchers who contract with meatpackers. It was the answer to decades of anguish among farmers and ranchers who endured unfair practices committed by corporate meatpackers. The USDA finalized its rules in December 2011, but unfortunately their efforts have been heavily attacked. Congress has blocked the implementation of the rule since 2012 through funding and continuing resolution bills. Even though Congress again protected USDA’s authority in the 2014 Farm Bill, the fight still goes on.

At their most robust, before being stripped, rescinded or blocked by Congress, the GIPSA rules included provisions to:

- Establish that a farmer who shows an injury from an unfair practice does not also need to show a competitive injury to the broader marketplace;

- Define “undue or unreasonable preference or advantage”;

- Require processors to maintain written records on differential pricing or data used to calculate farmers’ pay and to provide farmers with information about their pay upon request;

- Block packers from buying livestock from each other or a buyer from representing multiple packers at an auction, practices that effectively eliminate competitive bidding;

- Increase market transparency by requiring companies to provide sample contracts to USDA, made available to the public;

- Require live poultry dealers to set a base payment for all growers raising the same type of poultry and prohibit tournament or ranking systems that lower base payments;

- Make poultry companies give farmers at least 90 days notice before suspending bird delivery;

- Block processors from requiring farmers to make unnecessary expensive capital upgrades;

- Require contracts long enough to allow growers to recoup 80% of their capital investments;

- Give farmers a reasonable time to remedy a breach of contract before termination;

- Require contracts to clearly state that a producer has the right to decline a contract requiring arbitration and to include criteria for meaningful and fair participation in arbitration; and

- Prohibit retaliation against farmers for exercising their right to free speech and association, including talking to government officials about their contracts or abusive practices.

The Situation Today

Opposition to the GIPSA rules has come from major meatpackers and poultry processors like Tyson, Perdue, Cargill and Swift, as well as trade associations and corporate front-groups like the American Meat Institute, National Pork Producers Council and the National Chicken Council. Now that the USDA’s authority to issue the rules has been restored, it remains unclear which rules will be final, which will be scrapped and which will need additional comments and revisions.

The Dairy Industry

Several dynamics make the dairy industry ripe for manipulation by corporate players and make dairy farmers particularly vulnerable to unfair pricing.

Today just two firms, Dean Foods and Dairy Farmers of America (DFA), dominate the fluid milk sector, controlling most of the milk processed and marketed nationwide. While the national concentration ratio hovers around 30%, milk markets are heavily regional due to marketing order regulations and milk’s perishable nature. Regional markets are highly concentrated. Dean Foods controls 90% of the fluid milk market in the state of Wisconsin, 90% in Michigan, 70% in New England and between 70 and 90% in several other states.[2] Meanwhile, DFA controls about a third of the nation’s raw milk supply.[3]

The forces of supply and demand have little to do with the price dairy farmers receive from processors. The price is also unrelated to what consumers pay at the grocery store, nor is it based on a farmer’s cost of production or the supply of milk on the market. Instead, fluid milk prices are dictated by a convoluted formula based on the price of block cheddar cheese on the Chicago Mercantile Exchange (CME), even though less than 1% of U.S. cheddar is traded there.

The CME has a reputation for collusion and price gouging. In August 2006, the U.S. Department of Justice completed a two-year investigation of competition in the dairy industry, recommending action against Dean Foods, DFA and the now-defunct National Dairy Holding. In 2008, DFA agreed to pay $12 million to settle accusations by the CFTC that it manipulated block cheddar prices to boost the value of their futures contracts.[4] Both Dean and DFA have repeatedly been the targets of federal class action lawsuits [5] for colluding to suppress milk prices for farmers and prohibit other firms from entering the market.

Dairy farmers run operations that produce milk daily and thus, can lose substantial money each day if prices fall below their cost of production. In 2009, Dean Foods reported record first-quarter profits of $76.2 million – a 147.4% increase over its 2008 first-quarter profits. Meanwhile, prices to dairy farmers crashed by 40% and consumer milk prices barely budged. Dairy farmers face similar circumstances today, and many are again approaching the brink of bankruptcy. Between 1987 and 2007 the number of U.S. dairy farms decreased from 202,000 to 70,000 farms – a 65% decline.[6] The rural economies that depend on dairy farms cannot afford to see more farmers leave the land.

The Situation Today

Farm Aid and several of our partners continue to advocate for dairy pricing reform and antitrust investigation into the dairy sector. Dairy farmers need a floor price that covers their cost of production, not one based on the easily manipulated Chicago Mercantile Exchange. They need the government to investigate anti-competitive behavior by dairy processors and follow up on the investigations it has started or completed without comprehensive action.

The Seed Industry

Since the commercial introduction of GMOs in 1996, the seed industry has rapidly consolidated. Hundreds of independent seed dealers have gone out of business or been bought out and today just four companies control almost 60% of the seed market. For certain crops, the market is even more concentrated. The “big four” seed companies – Monsanto, DuPont, Syngenta and Dow – own 80% of the corn and 70% of the soybean market.

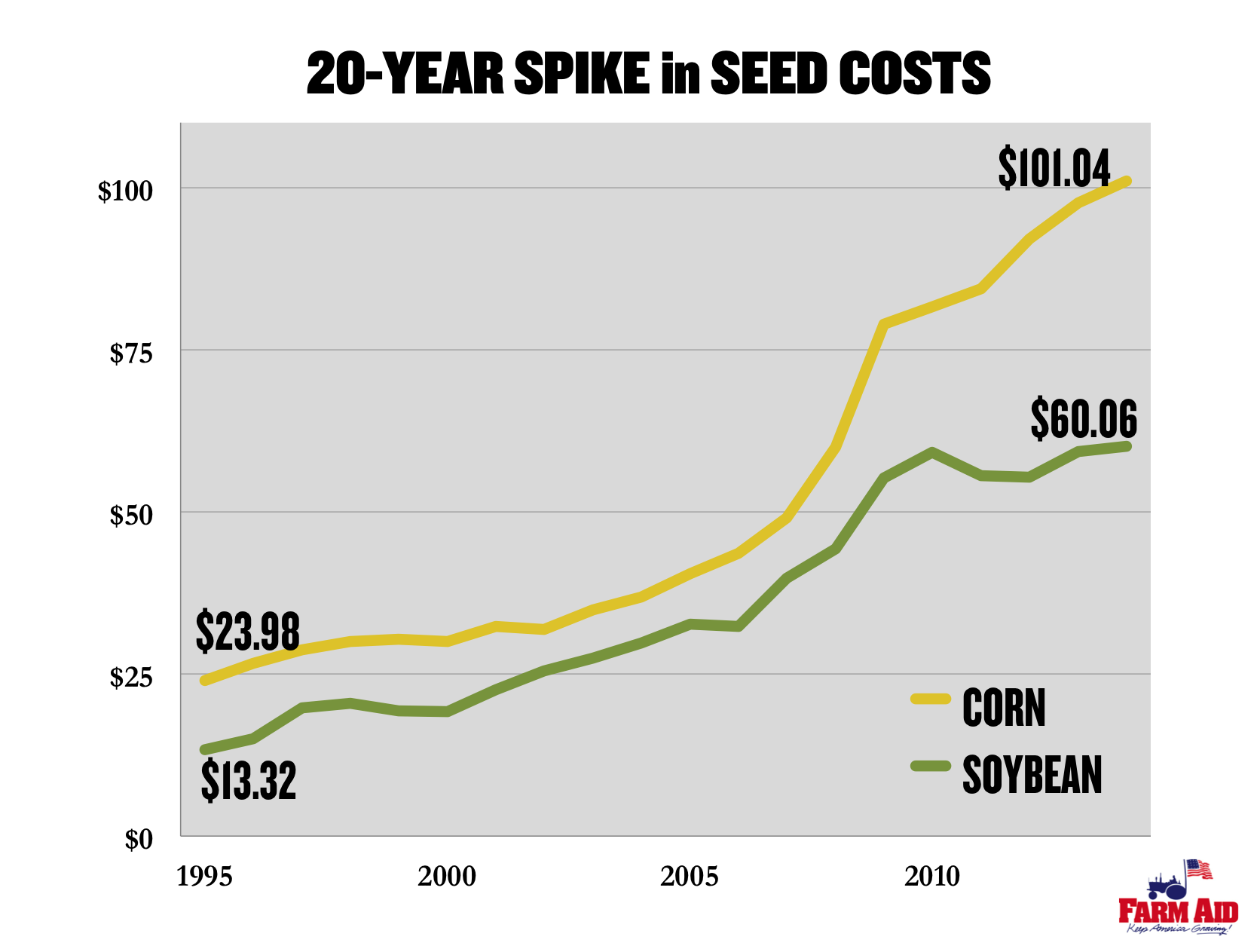

This concentration has made a huge dent in farmers’ pockets. USDA data show that the per-acre cost of soybean and corn seed spiked dramatically between 1995 and 2014, by 351% and 321%, respectively.[7] Those costs far outpaced the market price farmers received for corn and soy, leaving them tighter margins on which to run their farms.

Patents are also a critical dynamic in the seed industry. It wasn’t until the 1980s that GMOs could be patented, but patents are now key to furthering the power and profits of biotech companies. Farmers who buy GMO seeds must pay licensing fees and sign contracts that dictate how they can grow the crop – and even allow seed companies to inspect their farms. GMO seeds are expensive and farmers must buy them each year or else be liable for patent infringement. And while contamination can happen through no fault of their own, farmers have been sued for “seed piracy” when unauthorized GMO crops show up in their fields.

The Situation Today

Right now, pending mergers between Dow and DuPont as well as ChemChina and Syngenta could have devastating impacts on the already consolidated seed sector. Extreme consolidation in the seed industry has also coincided with the decline of public investment in traditional seed and breed development. Traditional breeding strategies can be very effective for complicated traits like drought resistance that involve more than one gene. At a time when farmers need more options, not fewer, these programs need to be bolstered.

Sources

- 1. Monroe, M. (2009) Milk brand choices slim as skim: Sanders calls for Dean Foods, DFA probe. St. Albans Messenger. St. Albans, Vermont. August 8, 2009.

- 2. Burnett, J. (2009) Independent Farmers Fell Squeezed by Milk Cartel. All Things Considered. National Public Radio. August 20, 2009.

- 3. Fitzgerald, A. (2010) Why Dairy Farmers are in a Sour Mood: Market dominance and possible manipulation hit milk prices. Business Week. May 27, 2010.

- 4. DFA class action lawsuit approaches settlement for Northeast farmers. Progressive Dairyman. February 19, 2015.

- 5. Gould, B.W. (2010) Consolidation and Concentration in the U.S. Dairy Industry. Choices Magazine. Agricultural & Applied Economics Association. http://www.choicesmagazine.org/magazine/article.php?article=123.

- 6. USDA ERS. Per-acre seed costs from Commodity Costs and Returns. http://www.ers.usda.gov/data-products/commodity-costs-and-returns.aspx.

- 7. Hendrickson, M., Heffernan, W.D. (2007) Concentration of Agricultural Markets. Columbia, MO, Department of Rural Sociology, University of Missouri. April 2007.

– Last updated: April 15, 2016 –

Click here to download this page as a PDF document for easy printing